Thinking of applying for a holiday loan? Here’s a rundown of everything you need to know about spreading the cost of that much-needed getaway.

You just can’t beat the excitement of stepping off the plane and jumping in a cab to the hotel. That first ice-cold drink by the pool and the prospect of time away from the noise of everyday life? Nothing compares.

In fact, studies show that travelling makes you calmer and less stressed and that feeling lasts for weeks (even when you’re back in the office).

But those benefits don’t last all that long if you get hit with hefty holiday loan repayments the moment your return flight lands.

With the cost of pretty much everything on the rise, two-thirds of Brits struggle to afford holidays abroad. So it’s no surprise that about 20% of people use credit cards to pay for holidays and more and more are turning to other finance options like holiday loans.

If you’re planning your next holiday and wondering if borrowing money with a holiday loan is the right choice for you, you’re in the right place. We’ve picked the Vuelo team’s brains on holiday loans and put together everything you need to know about them.

By the end of this quick guide, you’ll be able to book your next getaway and know you’ll come back worry-free (and with an incredible tan, hopefully).

Jump to a section

Get to know holiday loans and their risks

Everyone needs a holiday, in fact, research shows that we should all probably go on more than one holiday a year for our mental well-being. Holidays are a chance to take a step back, relax, and forget about everyday life. But with the cost of everyday life rising, it’s more difficult to pay for holidays in one lump sum.

That’s where holiday loans (and other options) come into their own.

If you want to borrow money for a holiday, holiday loans are pretty much what they say on the tin. They’re a type of personal loan that is specifically for helping people afford holidays.

In more technical terms, a holiday loan is an unsecured (meaning you don’t need to put up any collateral) personal loan that lets you split the cost of your trip. They’re designed for anyone who doesn’t have all the money upfront or would rather split the payments over a longer period.

How a holiday loan works:

- You borrow an amount, usually between £1,000 to £15,000 to cover holiday costs

- Most holiday loans have fixed interest rates which means predictable monthly repayments

- Your repayment period will usually be somewhere between 1 and 5 years

- You don't need to put up any collateral for the loan

Holiday loan risks to keep in mind:

- With average personal loan rates of around 12.42% APR, you could end up paying significantly more than the original cost of your holiday

- If you struggle to keep up with your repayment schedule you may have to make extra payments for charges and your debt can mount up

- Unlike other options, most holiday loans don't offer much flexibility if you face financial difficulties later on

Vuelo safety verdict:

Fast, but risky long-term.

Holiday loans are a quick solution when you’re planning your dream trip. They can be a good solution for some people but the repayment process can add stress to your finances long after you get home.

If you’re thinking about getting a loan for a holiday, we highly recommend thoroughly researching your options and using a trustworthy holiday loan calculator. That way, you can see repayment costs and how interest affects your overall holiday costs before you get a holiday loan.

And even if you think a holiday loan could help and work for your personal circumstances, it’s not the only way to borrow money for a holiday.

Consider all of your holiday finance options before booking

When it comes to booking and paying for your holiday, it’s good to know all the ways you can borrow money to travel.

Unfortunately, not all holiday lending and financing options are created equal and while none are entirely risk-free, some come with significantly less risk.

We’ve put together the pros, cons, and risk levels of all of the most common ways to pay for a holiday ( so you can find one that works best for you.

2.1 Personal loans

A personal loan is a popular way to finance a holiday. They work in pretty much the same way as a holiday loan as it’s an unsecured loan but give you more flexibility. This means you can use it to pay for more than just your holiday if you choose to. (For example, you could borrow enough to pay for the holiday and renovate your kitchen.)

How a personal loan works

You borrow a set amount from a bank or lender, usually between £1,000 and £25,000, with a fixed interest rate. You pay your loan back in monthly instalments typically over 1 to 7 years. Because it's unsecured, you don't need any collateral, but your credit history and score matter, better credit means a better rate.

Pros

- Predictable repayments: Fixed monthly payments help with budgeting and some providers will allow a repayment holiday to postpone payments if you're in a bind.

- Flexible use: You can use the loan for more than just your holiday-maybe those new suitcases and outfits too.

- Larger borrowing amounts: You can usually borrow more compared to a credit card.

Cons

- Interest costs: The rates can be high, especially if your credit score isn’t ideal.

- Debt risk: It’s still a form of debt, and missed payments can impact your credit score.

- Early repayment fees: Some loans have penalties if you decide to pay off your loan early.

Vuelo safety verdict:

Reliable but comes with a risk of long-term commitment.

Personal loans can be a reliable way to pay for your holiday, especially if you’ve planned your budget. But they come with a long-term commitment, which can be a downside if your financial situation changes.

2.2 Credit Cards

Credit cards are a common go-to for holiday spending. They offer flexibility, and with the right card, you might even benefit from perks like travel insurance or reward points.

How credit card payments work:

You charge holiday expenses to your credit card and repay over time, either in full or in monthly instalments. Interest rates vary, but many cards have a grace period, meaning no interest is charged if you pay the balance off quickly.

Pros

- Flexible payments: You can choose how much to repay each month.

- Perks and rewards: Travel points, cashback, and travel insurance can sweeten the deal.

- Purchase protection: Many credit cards offer extra consumer protection on purchases.

Cons

- High interest rates: If you don’t pay off the balance quickly, interest can add up fast.

- Temptation to overspend: It’s easy to get carried away and spend more than you can afford.

- Early repayment fees: High credit usage can lower your credit score.

Vuelo safety verdict:

Flexible, but the interest can catch up with you if you’re not careful.

Credit cards are convenient but come with the risk of accumulating high-interest debt. But they’re a really good option if you can pay off the balance quickly and take advantage of perks.

2.3 Overdrafts

An overdraft is when your bank allows you to spend more money than you have in your account, essentially borrowing from your bank to cover expenses. It can be an easy way to manage unexpected costs while traveling.

How overdraft payments work

You agree with your bank on an overdraft limit, and if you dip into it, you’ll pay interest or fees on the amount you’re overdrawn. Some accounts offer interest-free overdrafts up to a certain limit, but this usually only applies for a limited time.

Pros

- Instant access: You can use an overdraft immediately if your bank balance runs low.

- Flexible repayment: There are no fixed repayment dates, you pay it off as you top up your account.

Cons

- High fees: Interest rates and daily fees can be high, especially if you exceed the arranged limit with most banks charging 35-40% interest.

- Unpredictable costs: The costs can quickly add up if you don’t clear the overdraft soon.

- Not a long-term solution: Overdrafts are designed for short-term borrowing, not financing big expenses like a holiday.

Vuelo safety verdict:

Useful short-term, costly long-term.

An overdraft can work for covering small gaps in your holiday budget, but the fees can add up quickly if not managed carefully. It’s far more suitable for emergencies rather than financing an entire holiday.

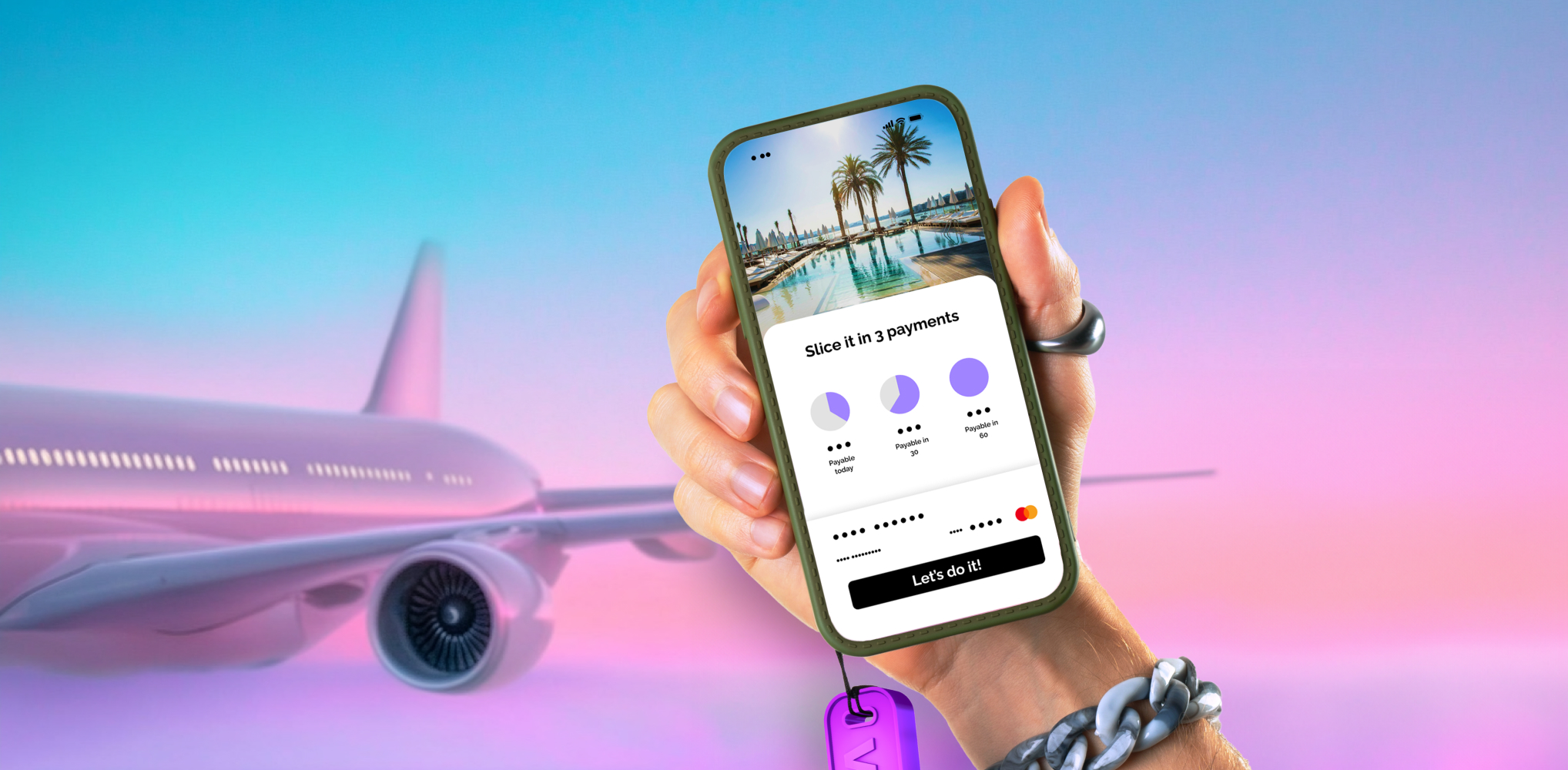

2.4 Buy Now Pay Later (BNPL)

Buy Now Pay Later services - like us, hey 👋 - let you split the cost of your holiday into manageable chunks, often with no interest if repaid on time. It’s a flexible option that has grown in popularity in recent years, especially for larger purchases like holidays.

How Buy Now Pay Later works

BNPL services like those offered through Vuelo allow you to book your holiday and pay in monthly instalments. Many BNPL options offer interest-free periods, which means you can spread the cost without additional charges, if you stick to the repayment schedule.

Pros

- Interest-free: Often, you can spread the cost with no interest if payments are made on time.

- Flexible repayment terms: You can choose a plan and loan term that suits your budget then set up a direct debit to pay it off, sometimes even after you come back from your trip.

- Quick approval: Easy and quick credit check process.

- Purchase protection: if there’s a problem with your holiday - say the hotel or airline goes out of business - you’ll get your money back, no questions.

Cons

- Late fees: Missing a payment can result in late fees and affect your credit score.

- Temptation to overspend: Spreading out the cost can make it easy to book something more expensive than you originally planned.

Vuelo safety verdict:

Useful short-term, costly long-term.

An overdraft can work for covering small gaps in your holiday budget, but the fees can add up quickly if not managed carefully. It’s far more suitable for emergencies rather than financing an entire holiday.

Get the app

At a glance: Your options to borrow money for a holiday

| Option | Pros | Cons | Vuelo Safety Verdict |

|---|---|---|---|

| Holiday Loans |

|

|

Fast but risky long-term |

| Personal Loans |

|

|

Reliable but requires a long-term commitment |

| Credit Cards |

|

|

Flexible, but the interest can add up fast |

| Overdrafts |

|

|

Useful for the short-term, costly long-term. |

| Buy Now Pay Later |

|

|

Safest option: flexible and interest-free |

The results: book everything from flights to hotels with Vuelo’s buy now pay later holiday payments and spread the cost over time

Taking out a loan for a holiday might seem like a good idea when you can’t wait to get away from the daily grind, but the repayment stress can linger long after your tan fades. Why let financial worries follow you home when there’s a better way to finance your dream getaway?

With Vuelo, you can enjoy all the benefits of booking your holiday now without the added stress of high-interest repayments. The Vuelo app makes it easy to find the cheapest flights, snag last-minute deals, and compare prices, all while giving you the flexibility to spread the cost over time.

Ready to change how you plan your holidays? Here’s how Vuelo helps:

- 💰 Spread the cost of your holiday without worrying about interest.

- 🙌 Save up to 48% by booking early and get money-saving tips to keep costs down.

- ✈️ Find the cheapest flight and hotels by comparing across multiple platforms.

- 📱 Book flights, hotels, and more from one easy-to-use app.

Ensure you can make repayments on time. You must be 18+ and a permanent UK resident. Vuelo charges a £12 late fee for each late instalment. Missed payments may affect your ability to use Vuelo in the future. Vuelo's Interest Free instalment agreements are not regulated by the Financial Conduct Authority. T&Cs and other eligibility criteria apply.

Download the Vuelo app

today to pay for your holiday without financial anxiety. Spread the cost over flexible interest-free payments.

Get the app